Jialang Wang via MR:

Benford’s law, also called the first-digit law, states that in lists of numbers from many (but not all) real-life sources of data, the leading digit is distributed in a specific, non-uniform way. According to this law, the first digit is 1 about 30% of the time, and larger digits occur as the leading digit with lower and lower frequency, to the point where 9 as a first digit occurs less than 5% of the time. This distribution of first digits is the same as the widths of gridlines on the logarithmic scale.

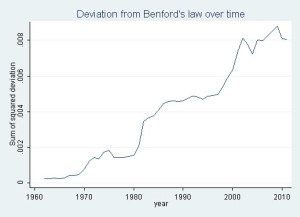

And from Jialang:

Deviations from Benford’s law have increased substantially over time, such that today the empirical distribution of each digit is about 3 percentage points off from what Benford’s law would predict. The deviation increased sharply between 1982-1986 before leveling off, then zoomed up again from 1998 to 2002. Notably, the deviation from Benford dropped off very slightly in 2003-2004 after the enactment of Sarbanes-Oxley accounting reform act in 2002, but this was very tiny and the deviation resumed its increase up to an all-time peak in 2009.

Looks like recessions are bad for corporate disclosure. Makes sense: if you can make the growth targets, you’re not worried. Once things get ugly, though…

But levels matter here, not rates. Why does it become entrenched?

I would love to find some time to apply this to insurance company data…