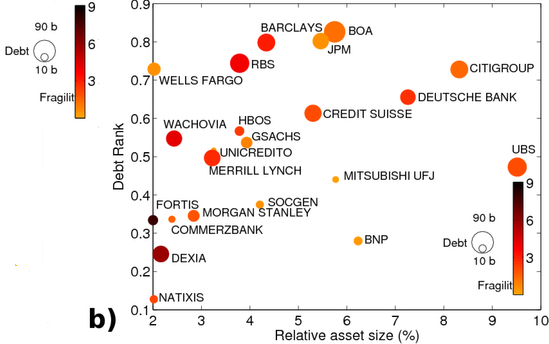

Systemic risk — the risk of default of a large portion of a financial system — depends on the network of financial exposures among institutions, but there is no widely accepted method for working out which institutions in a network are the most important to the stability of the system. Inspired by feedback-centrality measures in networks, such as PageRank, Stefano Battiston and colleagues introduce a new measure of systemic impact, which they call DebtRank. They use DebtRank to analyze a recently released data set with information on the institutions that received aid from the US Federal Reserve Bank through its US$1.2 trillion emergency loans programmes during 2008 to 2010.

The authors find that during the peak of the crisis, a group of 22 financial institutions, which received most of the loans, became more central to the network, which means that the default of each one would have a larger economic impact on the whole network. Even small, dispersed shocks to individual banks could thus have triggered the default of a large portion of the system. The authors note that because the network of impact used in the study is a proxy of the real, unknown network, the findings should be regarded with caution, but the study shows the kinds of insights that can be gained using DebtRank.

More here. Via Alex Tabarrok at MR who comments:

One point to note is that the authors calculated centrality using ex-post data from the Fed. Using this measure, DebtRank clearly signaled danger prior to the crisis and did so earlier than other metrics. In order to do this in real time, however, much more transparent and timely data would be necessary. The fact that centrality doesn’t correlate all that well with bigness, however, indicates that without this data the problem of monitoring risk is even more difficult than it appears.

I am impressed. Being able to distill an abstract concept like “interconnectivity” into a single number is extremely powerful. Politicians should latch onto this and legislate its calculation at reasonably frequent intervals.

Bailouts are a horrible, disgusting abomination. My first reaction to all this is that we should break out the pitchforks and treat high DebtRanking institutions real bad. Like they do in Texas.

And I will plug my ears lest I listen to too much of this kind of cowardly disclaimer:

The authors note that because the network of impact used in the study is a proxy of the real, unknown network, the findings should be regarded with caution