Samuel Arbesman points us to this paper that models the likelihood of a terrorist event. Reading through it quickly, I’m astonished that the authors didn’t bother to look up the actuarial literature on modeling extreme events, much less terrorism. There’s an entire exam dedicated to the methods these authors have ‘developed’.

Anyway, it’s interesting to see how a different approaches a topic I spend a lot of time thinking about and they don’t do too badly, picking the lognormal and an inverse transformed uniform distribution as their main tail estimators. We tend to us inverse gauss, which makes estimation a bit easier, but it’s the inverse transformation that gives the tail the juice.

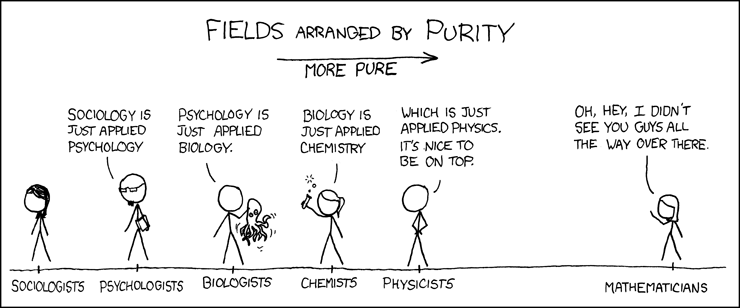

So where do actuaries fall in the xkcd purity scale?

Off the list, it seems, under: irrelevant.