Some time ago I was toying with the idea of opening a retail franchise. Now, I didn’t know a thing about retail, but I remembered one of my marketing professors was a retail specialist, so I emailed him. He suggested a textbook and I ordered it (older version because, come on, $120!?). Then, for the first time in my life, I read a textbook trying to learn rather than just get through a course.

Complete waste of time. No real advice on how to actually run a business. Instead, lots of features for memorizing a load of minimally useful jargon: summary bullets in the (large) margins, more bullet summaries at the end, narrative summaries, Q&A and very little actual advice.

I eventually passed on the franchise but was left with the impression that the academy has very little to offer business owners. So with that in mind, this article from the OECD has got me thinking of the big picture of my own business.

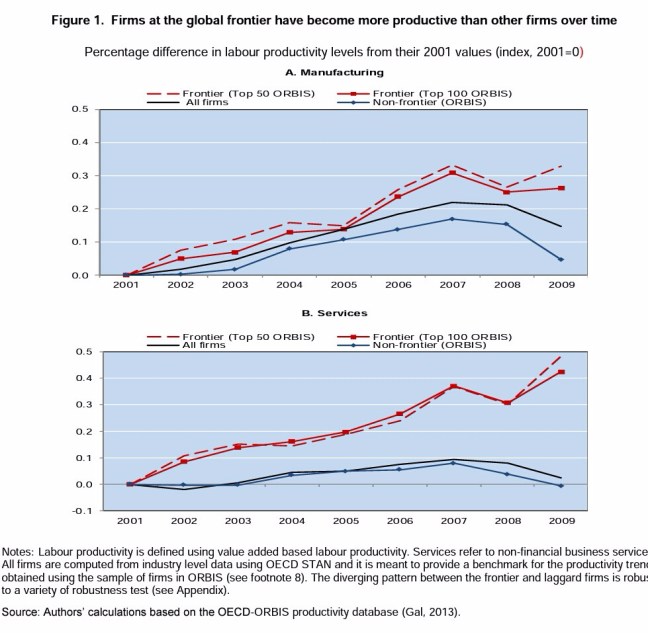

The core idea boils down to this graph, which charts the increasing gap between labor productivity of the top firms and the rest (note how much stronger this is in service firms):

They also note that the churn in firm rankings is dropping, too, so firms at the ‘global frontier’ are getting older and that

“..evidence from eight European economies suggests that MFP growth over the 2000s was weaker in sectors that recorded larger declines in the share of young firms (under 6 years), and in particular start-ups (under 3 years)”.

The authors like this explanation:

More importantly, the rising gap in productivity growth between firms at the GF and other firms since the beginning of the century suggests that the capacity of other firms in the economy to learn from frontier may have diminished [emphasis DW].

They go on quite a lot about how firms should learn from each other and that promoting this should be the key policy goal.

I don’t buy it.

Firms do learn (steal) from each other but I think the biggest difference in success is management’s desire and ability to take raw (stupid) ideas and turn them into great businesses. That is about high quality people, effective management, perseverance, passion. Those things aren’t any more scarce than they were 50 years ago.

Interestingly, there’s a hint of an explanation I much prefer in the paragraph following the quote above:

Firms at the global productivity frontier are typically larger, more profitable, and more likely to patent, than other firms. Moreover, they are on average younger, consistent with the idea that young firms possess a comparative advantage in commercialising radical innovations (Henderson, 1993; Baumol, 2002) and firms that drive one technological wave often tend to concentrate on incremental improvements in the subsequent one (Benner and Tushman, 2002). However, the average age of firms in the global frontier has been increasing since 2001 (Figure 12). To the extent that this reflects a slowdown in the entry of new firms at the global frontier, it could also foreshadow a slowdown in the arrival of radical innovations and productivity growth [emphasis DW].

The big point the authors miss here is that the large firms, which are themselves young, were once small firms that beat the frontier firms du jour. They did figure something out. Then they sat on that idea and mined it.

Thiel flagged top entrepreneurs such as Bill Gates, Larry Page, and Mark Zuckerberg as people who had built their businesses on unique ideas, and advised future innovators that, “if you’re copying these people, you’re not learning from them“.

Now I summon Horace Dediu:

What really causes a company to fail is disruption. The business model around which all products, customers and priorities are built; the culture, the skills and “DNA” of the company; is vulnerable. This vulnerability is why companies have considerably shorter lifespans than the people who work there. They are one of the most fragile of organisms: high infant mortality, with short, unpredictable lives.

Microsoft ascended because it disrupted an incumbent (or two) and is descending because it’s being disrupted by an entrant (or two). The Innovator’s Dilemma is very clear on the causes of failure: To succeed with a new business model, Microsoft would have had to destroy (by competition) its core business. Doing that would, of course, have gotten Ballmer fired even faster.

The key thing that Disruption Theory taught me is that profitable firms can’t make big changes. Management snuffs out the raw (stupid) ideas instead of building businesses with them. Their first priority is to protect the existing business which real disruption necessarily destroys. Any other innovation is called sustaining innovation, in that it can be adopted by incumbents, making them stronger, not weaker. So if I observe older firms and stagnant rankings my question is: why aren’t the younger firms innovating? Peter Thiel again (video):

It’s not a fact of nature that the slowdown has happened. We’ve become risk averse, we’re regulated to death, we’ve become incrementalist and we’re not really willing to take bold steps. We’ve talked ourselves into thinking that throwing angry birds at pigs is the best we can do.

“We” don’t want innovation? I think that’s right, actually.

There happens to be an enormous amount of confusion over disruption in insurance circles because people think you’re talking about the periodic purge of the market cycle. The laggard firms do tend to take a lot more damage during cycle turns and cyclical startups do tend to use the newest tech so cyclicality acts as an accelerant for innovation. The fact remains, though, that the cycle of the insurance business is much more powerful in the short term (ie for your career) than innovation. The vast majority of startup firms in insurance businesses owe their scale to good cycle timing.

The average culture is thus highly aware of cyclical change but under-appreciates structural change. I work at a small company, dwarfed by our competitors by 10x, 100x, 500x and I see every day how the large organizations are slower to react to new ideas than we are. They can’t jeopardize that existing business! So though it makes me feel good to say that we are leaders in much of what we do, quicker to invent, quicker to adopt, we feel our lack of resources all the time and resources have been enough to keep the incumbents entrenched. They do a good enough job! No innovation we’ve led has been so novel that our competitors can’t either steal it or ignore it and cede to us the moderate growth that rewards moderate innovation.

But moderate innovation is still something and we’ve capitalized on maturing technologies in data capture, storage and analytics. These are sustaining innovations so everyone benefits but they’ve still been transformational on a longer time scale.

Back in the dark ages, decisions were made at the hyper-local level and only consolidated for financial reporting purposes. Large organizations could not be centrally controlled because it was too expensive to answer any question other than: are we making an accounting profit?

So they had a culture of delegated decision making: independent, proud, cunning and highly social. Deals were done on the proverbial napkin because a low oversight, high trust relationship meant mistakes could be corrected or swept under the rug with ‘special deals’ later on.

Then technology facilitated oversight and accountability from a distance. People who could manage systems and build models to oversee operations were suddenly empowered at the expense of grass roots freedom. This concentration of information (power) enabled a wave of consolidation, snuffing out the need for individuals to manage external relationships. Less freedom, more oversight, less (individual) trust, more transparency. We all became a bit more corporate and the culture changed.

My story is that this drove the consolidation of reinsruance brokers, too. Back in the old days, an individual broker would spend half his career working for someone else, building up a book and then selling that book to a bidding firm or starting his/her own shop. The individual relationship was what mattered. Today the value of those relationships is significantly eroded. Business is ‘corporatized’, more services are required and a whole hierarchy of relationships are needed to manage the hierarchy at client and counterparty organizations. The actual change has been long and painful, yet the firms that remain are mostly the same ones that we started with, excepting for a whole lot of M&A.

Now we can test the OECD observations and analysis against my experience.

- Are the small firms lagging behind the large ones? Check.

- Is the gap widening. Yep, probably.

- Is it because they can’t learn from the large firms? No, I don’t think so.

I think small firms are disappearing because the industry wants scale to supply capital-intensive and relationship-intensive services. Small firms generally have the same ideas as the big firms but they just lack the resources to implement them. To win (survive), small firms need to have better ideas.

My company has been different from other small firms in that we’ve been able to implement new ideas that large firms haven’t. We have a superior process. But our ideas haven’t been powerful enough to unseat the megas in a meaningful way.

Scale rewards itself and it’s hard to break into that virtuous cycle. M&A works, but it is difficult not to revert to the cultural mean doing that. And scale the ‘easy’ way yields the most stagnant of entities: constantly fighting over itself. Maybe most importantly of all, there are very few small firms still in existence in my business, so nobody to buy.

And that’s the key feature that the OECD report misses. Something is different out there that is killing startups before birth. I say increasing rewards to scale have kept smaller firms from getting a seat at the table.

The market prefers scale to the innovations it’s been presented.