This post is part of the social science of insurance series

Nobody Cares About Insurance, Neither Do You

It is common to confuse why insurance exists with why customers buy it. I’ve spent much of my career trying to convince people to spend real money on risk management and am frequently surprised at how little they care, even when they purchase! This essay is about why that is, what actually motivates insurance purchases and what the implications are for sellers and manufacturers of insurance products. Agents, brokers, underwriters, entrepreneurs and investors, please stop trying to talk customers into buying insurance. They don’t want it.

Where It All Goes Wrong

When I sold insurance I noticed prospects almost always asked: “How can I make money on this?”

Reliably making money on insurance is a silly idea of course. Buying insurance isn’t a business opportunity, it’s a service you pay for that, in order to exist, is overwhelmingly likely to give you nothing back.

Yet we instinctively seek to profit off insurance. I was asked this question while selling health insurance to consumers and while selling corporate insurance ‘treaties’ to multinational insurance companies. I was astonished that the most and least sophisticated buyers of insurance all started from the same place and followed similar paths.

Nobody wants to pay for insurance when they get nothing back and by this measure, insurance never sounds like a great deal: “I pay you money today so you can pay me nothing later”? Why would anyone do this?

The reason is a bit messy to explain. You should buy it because you are underprepared for financial volatility.

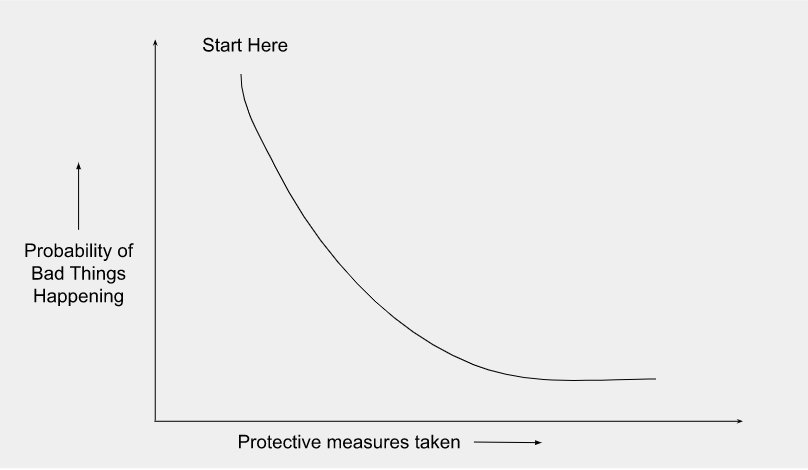

Our lives start with lots of risk and no protection and we somehow decide what risks to focus on through avoidance, mitigation and insurance. You’ll notice, though, that you’re never done with risk no matter how much resource you throw at it. So while there is such a thing as spending too little on protection one can also overdo it.

While visiting family in Ontario I heard a story of a person living illegally on an undeveloped island in the St Lawrence River who would rant at boater passersby about how civilization will imminently collapse (in this case because of COVID-19). This was a person obsessed with risk and willing to spend every available resource to avoid it1. Of course most of us err on the other side, of buying too little insurance and canceling it too readily. Why these errors?

Cognitive Bias and Insurance

Humans have some predictable blind spots when making decisions called cognitive biases. Even though I think the label is overused2, biases are easy to spot in people who buy insurance. I’ve observed systematic behavior that, if it were not corrected, is incompatible with a functioning insurance market.

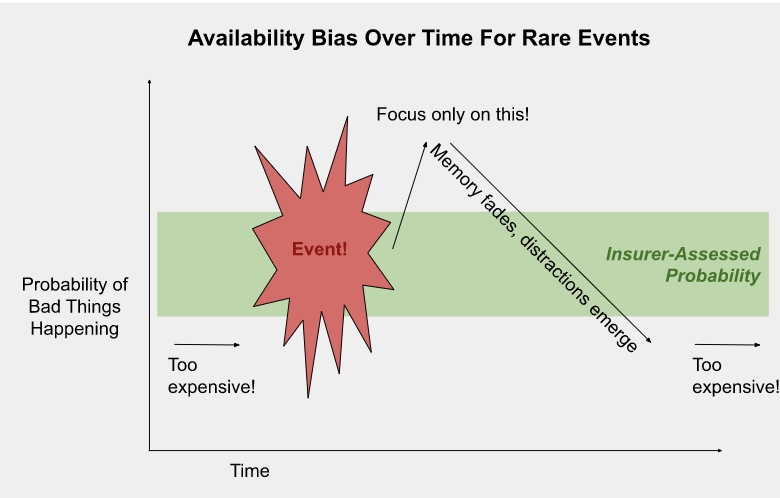

Availability bias, for example, roughly means “I believe what I see”. This makes insurance for things we haven’t experienced look expensive. Once we do experience something bad, availability bias causes us to overcorrect. Smart insurers are happy to sell to newly risk conscious customers. But some customers will take that to the extreme and still not buy because they think they can eliminate their risk entirely by mitigation, think of our friend in the St Lawrence River.

Availability bias is also a fickle master: memories fade and our limited focus gets distracted by the next crisis or the one after3. Eventually we find other needs for the resources devoted to mitigation and let insurance coverage lapse.

On top of that, a slew of egocentric biases impede the purchase of coverages designed to protect folks other than the insured. This forms a surprisingly large share of the insurance industry. One example is life insurance, which doesn’t benefit the buyer one bit. Another is liability insurance, which protects others from damages caused by the buyer. When we cause harm to someone there are strong social norms for making it up to the victim. Harm a stranger, though, and who’s going to know? Why would we buy liability insurance to help these people?

These are the psychological hurdles a large, complex insurance industry needs to overcome: 1) our deficiency in understanding probabilities, especially of bad events, confuses us into buying too little and the wrong kinds of insurance; 2) an overreaction to new information causes us to non-renew coverages when our focus wanders; and, 3) an aversion to fulfilling obligations to others, particularly distant strangers, which limits the size of groups we can integrate with socially and economically.

How Culture Works (For Insurance)

Let’s go back to our crazy friend on the St Lawrence River. Does his mom know he’s out there? Our inner circle usually blunts our wackier impulses and weighs in heavily on really tough decisions, especially those involving risk. These decisions become social decisions, which are more rational than individual decisions4 because groups are able to 1) incorporate larger amounts of information in decisions and 2) cohere on a shared set of stable, often more self-interested, preferences.

An interesting feature of social decisions is that they are hard to circumvent. Disobeying the consensus might get you thrown out of the group. We rely a lot on our groups, for a sense of belonging like having family dinner, and for more material benefits of financial support in times of hardship. That cultural evolution has tied these social benefits, literally the most important features of human life, to social conformity is a powerful signal for how important obeying social decisions is to survival. And social decisions don’t end with mom, the concept extends to larger scales. Anthropologist Joe Henrich argues in his book The Secret of Our Success that we are genetically evolved to learn by copying others in a process called cultural learning. We do not understand and do not need to understand why certain behaviors are wise or efficient; we merely have to adopt the behaviors modeled by high status, successful members of society. Culture, in other words, gives us the power to override our cognitive biased-addled minds. Cultural rules can take many forms, including legislation, but informal cultural norms regulate insurance as well. The most important characteristic of these norms is that we follow them, even if we hate them.

How We Actually Make Insurance Decisions

Henrich has documented a variety of cultural innovations in the last two millennia, like gods punishing contract breakers and bans on cousin marriage, that have gradually deposed the kin group as the primary mediator of trust in Western societies. This innovation was very successful. Cultures that can coordinate millions of members are at an incredible competitive advantage over those restricted to trusting the thousands of people in a kin group.

The insurance manifestation of that competitive advantage is the aggregation of information from everyone’s experiences to gain knowledge about which risks are common and which are not. This allows us to better identify one-offs and also protect people against risks they may never have imagined. We don’t, however, get a definitive answer for what risks to prioritize, the best we can do is study the emergent outcome of cultural evolutionary processes.

These processes usually feel slow. Let’s say in the distant future Tijuana has more strictly mandated flood mitigation and insurance practices than San Diego. Then a giant flood strikes both. San Diego, embarrassed at losing more life and property, might change its tune quickly and copy Tijuana. Conversely, if no flood occurs for decades or centuries San Diego will probably have much nicer waterfront development and immigrants or tourists coming to enjoy it, fueling higher economic growth. Meanwhile politicians in Tijuana will likely be mulling the value of the ‘red tape’ holding them back. That’s cultural evolution.

This process is actually no different than that of availability bias that I maligned earlier: updating probabilities based on experience. The difference is that cultures integrate vastly more information over longer time periods, sometimes exceeding human lifetimes. And in insurance, where compulsion to purchase is the norm, we see that the worse our individual decision making processes are, say in preparing for unlikely but consequential events or in trusting distant economic agents, the more powerful our group controls are.

So What Do We Do?

Taking the question back up of how to sell insurance, you can almost ignore the buyer. The real customer is the group of people that will force a purchase for the greater good. Here are some takeaways for different groups of people in the insurance value chain.

Insurance Salespeople (Agents, Brokers)

Key questions:

- What/Who is forcing this person to buy? What do these tyrants want?

- Whose behavior should the buyer be copying and why?

The second question gives an opening to actually influencing the buyer through social validation, a less direct form of compulsion than a law or contractual mandate and correspondingly less effective.

Underwriters and Product Designers

Key questions:

- What is the minimum requirement?

- If customers buy more, why?

Keep in mind: bolt-ons and upsells that solve a unique client problem are usually high margin. If this is voluntary coverage, expect lapses!

Ambitious Entrepreneurs and Investors

I have in mind those who wish to build entire new insurance systems and products. To them I say: focus on the beneficiary of insurance, not the insured. Then empower that beneficiary to compel insureds to purchase.

The Bottom Line

The insurance system is based on a kind of relational violence, of bending people’s behavior towards the commonweal. Maybe you, like I, don’t really like that fact. But it’s the best way humanity has come up with to protect itself.

Footnotes

1 Of course he was disregarding certain risks of personal injury and… hygiene.

2 Wikipedia lists maybe a hundred? https://en.wikipedia.org/wiki/List_of_cognitive_biases

3 Take this to the limit and you get “on demand insurance” where people buy insurance “while they need it”. This increases the threat of moral hazard, however, so only works for some products and markets.

4 Social decisions often better conform to some definitions of rationality. See: Kugler, Tamar, Edgar E. Kausel, and Martin G. Kocher. “Are groups more rational than individuals? A review of interactive decision making in groups.” Wiley Interdisciplinary Reviews: Cognitive Science 3.4 (2012): 471-482.