Brian has been at the center of two massive social shifts in the last 20 years, first the investigation of implicit bias and second the replication crisis in social sciences.

What did I learn?

Incredibly, I had underestimated Brian Nosek! His real contribution was to build technology that massively reduced the cost of conducting empirical studies, paving the way to increased power for studies and massively easier efforts at replication.

What was my favorite part?

“People aren’t happy to get an email from me” he says. Mostly if you are a researcher and get a cold email from Brian it means he’s about to put your research to the replication test. Better be real!

There you are, proud a journal published your result after years of effort.. Then an email appears: Hi I'm @BrianNosek and I'm going to try to figure out if that was all for real Not everyone is happy to get this email! Continue watching our conversation: https://t.co/LDuAdSHAnEpic.twitter.com/LldrUKq3gy

It is common to confuse why insurance exists with why customers buy it. I’ve spent much of my career trying to convince people to spend real money on risk management and am frequently surprised at how little they care, even when they purchase! This essay is about why that is, what actually motivates insurance purchases and what the implications are for sellers and manufacturers of insurance products. Agents, brokers, underwriters, entrepreneurs and investors, please stop trying to talk customers into buying insurance. They don’t want it.

Where It All Goes Wrong

When I sold insurance I noticed prospects almost always asked: “How can I make money on this?”

Reliably making money on insurance is a silly idea of course. Buying insurance isn’t a business opportunity, it’s a service you pay for that, in order to exist, is overwhelmingly likely to give you nothing back.

Yet we instinctively seek to profit off insurance. I was asked this question while selling health insurance to consumers and while selling corporate insurance ‘treaties’ to multinational insurance companies. I was astonished that the most and least sophisticated buyers of insurance all started from the same place and followed similar paths.

Nobody wants to pay for insurance when they get nothing back and by this measure, insurance never sounds like a great deal: “I pay you money today so you can pay me nothing later”? Why would anyone do this?

The reason is a bit messy to explain. You should buy it because you are underprepared for financial volatility.

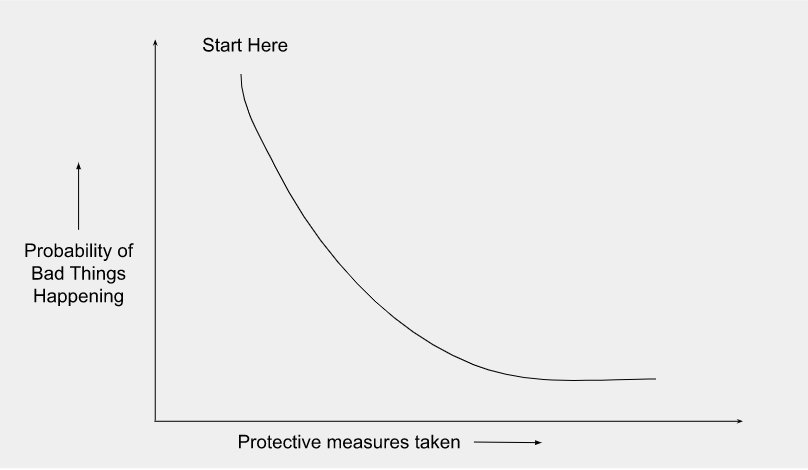

Our lives start with lots of risk and no protection and we somehow decide what risks to focus on through avoidance, mitigation and insurance. You’ll notice, though, that you’re never done with risk no matter how much resource you throw at it. So while there is such a thing as spending too little on protection one can also overdo it.

While visiting family in Ontario I heard a story of a person living illegally on an undeveloped island in the St Lawrence River who would rant at boater passersby about how civilization will imminently collapse (in this case because of COVID-19). This was a person obsessed with risk and willing to spend every available resource to avoid it1. Of course most of us err on the other side, of buying too little insurance and canceling it too readily. Why these errors?

Cognitive Bias and Insurance

Humans have some predictable blind spots when making decisions called cognitive biases. Even though I think the label is overused2, biases are easy to spot in people who buy insurance. I’ve observed systematic behavior that, if it were not corrected, is incompatible with a functioning insurance market.

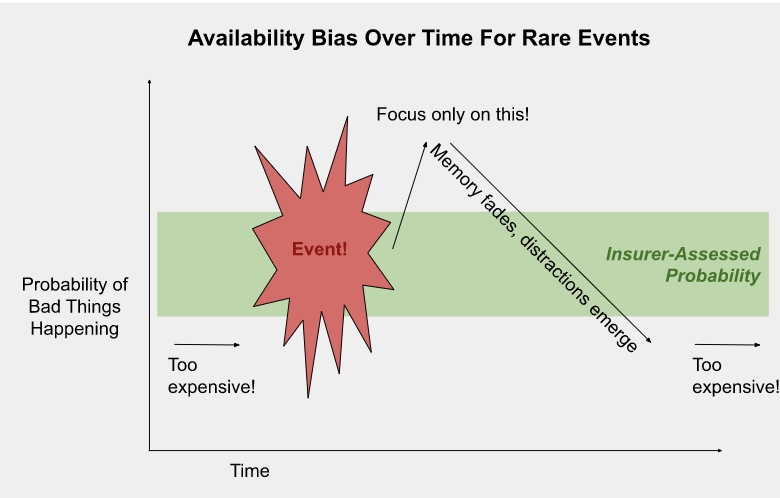

Availability bias, for example, roughly means “I believe what I see”. This makes insurance for things we haven’t experienced look expensive. Once we do experience something bad, availability bias causes us to overcorrect. Smart insurers are happy to sell to newly risk conscious customers. But some customers will take that to the extreme and still not buy because they think they can eliminate their risk entirely by mitigation, think of our friend in the St Lawrence River.

Availability bias is also a fickle master: memories fade and our limited focus gets distracted by the next crisis or the one after3. Eventually we find other needs for the resources devoted to mitigation and let insurance coverage lapse.

On top of that, a slew of egocentric biases impede the purchase of coverages designed to protect folks other than the insured. This forms a surprisingly large share of the insurance industry. One example is life insurance, which doesn’t benefit the buyer one bit. Another is liability insurance, which protects others from damages caused by the buyer. When we cause harm to someone there are strong social norms for making it up to the victim. Harm a stranger, though, and who’s going to know? Why would we buy liability insurance to help these people?

These are the psychological hurdles a large, complex insurance industry needs to overcome: 1) our deficiency in understanding probabilities, especially of bad events, confuses us into buying too little and the wrong kinds of insurance; 2) an overreaction to new information causes us to non-renew coverages when our focus wanders; and, 3) an aversion to fulfilling obligations to others, particularly distant strangers, which limits the size of groups we can integrate with socially and economically.

How Culture Works (For Insurance)

Let’s go back to our crazy friend on the St Lawrence River. Does his mom know he’s out there? Our inner circle usually blunts our wackier impulses and weighs in heavily on really tough decisions, especially those involving risk. These decisions become social decisions, which are more rational than individual decisions4 because groups are able to 1) incorporate larger amounts of information in decisions and 2) cohere on a shared set of stable, often more self-interested, preferences.

An interesting feature of social decisions is that they are hard to circumvent. Disobeying the consensus might get you thrown out of the group. We rely a lot on our groups, for a sense of belonging like having family dinner, and for more material benefits of financial support in times of hardship. That cultural evolution has tied these social benefits, literally the most important features of human life, to social conformity is a powerful signal for how important obeying social decisions is to survival. And social decisions don’t end with mom, the concept extends to larger scales. Anthropologist Joe Henrich argues in his book The Secret of Our Success that we are genetically evolved to learn by copying others in a process called cultural learning. We do not understand and do not need to understand why certain behaviors are wise or efficient; we merely have to adopt the behaviors modeled by high status, successful members of society. Culture, in other words, gives us the power to override our cognitive biased-addled minds. Cultural rules can take many forms, including legislation, but informal cultural norms regulate insurance as well. The most important characteristic of these norms is that we follow them, even if we hate them.

How We Actually Make Insurance Decisions

Henrich has documented a variety of cultural innovations in the last two millennia, like gods punishing contract breakers and bans on cousin marriage, that have gradually deposed the kin group as the primary mediator of trust in Western societies. This innovation was very successful. Cultures that can coordinate millions of members are at an incredible competitive advantage over those restricted to trusting the thousands of people in a kin group.

The insurance manifestation of that competitive advantage is the aggregation of information from everyone’s experiences to gain knowledge about which risks are common and which are not. This allows us to better identify one-offs and also protect people against risks they may never have imagined. We don’t, however, get a definitive answer for what risks to prioritize, the best we can do is study the emergent outcome of cultural evolutionary processes.

These processes usually feel slow. Let’s say in the distant future Tijuana has more strictly mandated flood mitigation and insurance practices than San Diego. Then a giant flood strikes both. San Diego, embarrassed at losing more life and property, might change its tune quickly and copy Tijuana. Conversely, if no flood occurs for decades or centuries San Diego will probably have much nicer waterfront development and immigrants or tourists coming to enjoy it, fueling higher economic growth. Meanwhile politicians in Tijuana will likely be mulling the value of the ‘red tape’ holding them back. That’s cultural evolution.

This process is actually no different than that of availability bias that I maligned earlier: updating probabilities based on experience. The difference is that cultures integrate vastly more information over longer time periods, sometimes exceeding human lifetimes. And in insurance, where compulsion to purchase is the norm, we see that the worse our individual decision making processes are, say in preparing for unlikely but consequential events or in trusting distant economic agents, the more powerful our group controls are.

So What Do We Do?

Taking the question back up of how to sell insurance, you can almost ignore the buyer. The real customer is the group of people that will force a purchase for the greater good. Here are some takeaways for different groups of people in the insurance value chain.

Insurance Salespeople (Agents, Brokers)

Key questions:

What/Who is forcing this person to buy? What do these tyrants want?

Whose behavior should the buyer be copying and why?

The second question gives an opening to actually influencing the buyer through social validation, a less direct form of compulsion than a law or contractual mandate and correspondingly less effective.

Underwriters and Product Designers

Key questions:

What is the minimum requirement?

If customers buy more, why?

Keep in mind: bolt-ons and upsells that solve a unique client problem are usually high margin. If this is voluntary coverage, expect lapses!

Ambitious Entrepreneurs and Investors

I have in mind those who wish to build entire new insurance systems and products. To them I say: focus on the beneficiary of insurance, not the insured. Then empower that beneficiary to compel insureds to purchase.

The Bottom Line

The insurance system is based on a kind of relational violence, of bending people’s behavior towards the commonweal. Maybe you, like I, don’t really like that fact. But it’s the best way humanity has come up with to protect itself.

Footnotes

1 Of course he was disregarding certain risks of personal injury and… hygiene.

3 Take this to the limit and you get “on demand insurance” where people buy insurance “while they need it”. This increases the threat of moral hazard, however, so only works for some products and markets.

4 Social decisions often better conform to some definitions of rationality. See: Kugler, Tamar, Edgar E. Kausel, and Martin G. Kocher. “Are groups more rational than individuals? A review of interactive decision making in groups.” Wiley Interdisciplinary Reviews: Cognitive Science 3.4 (2012): 471-482.

This conversation gave me such a feeling of humility yet hope about our world. It’s an awful place sometimes but some people are truly awesome at making it better.

Jen Brady is the Executive Director of Oasis, a non-profit serving women and children in Paterson, NJ and this is her second appearance on the show. In the first show we talked about COVID and the poor. This time we’re digging right onto Oasis and its mission and how it’s doing.

Charity is incredibly similar to insurance. As I half joked once in comparing them: “One of them supplies resources to those in desperate need and hopefully enables them to pull themselves out of their difficult circumstances to lead a successful life. So does the other one.” Insurers could do well to learn from Jen. And she has a remarkable track record, doubling the size of Oasis during her tenure and initiating many fascinating experiments and new initiatives in Paterson, NJ.

We discuss: * How self-belief is the most important factor in women lifting themselves out of poverty * How that feeling of self-belief is constructed, influenced and nurtured in and out of Oasis * The difference between generational poverty and immigrant poverty * What is the drop out rate (I was astonished) and how do they manage drop-outs * Do the problems feel endless? * What did they learn by extending Oasis into housing development? * How to not create bureaucracy in solving problems * How they handle the cultural complexity of women and children from 26 different countries (plus Paterson natives!) * How the social consequences of COVID (lockdowns, etc) impacted poor families * How much talent there is hidden in places like Paterson

Why did I do this show?

Jen Brady (https://oasisnj.org/) is a tremendously successful executive in an industry (non-profit) that I know virtually nothing about but which has a very many links to my insurance.

What did I learn?

A very many things. One that nearly everyone who enters these programs drops out. Working with that fact in a graceful way to bring people in and out is a cornerstone of succeeding at the very difficult work Oasis does.

What was my favorite part?

I was delighted to hear about all the experiments they’r running at Oasis and generally how similar the problems of delivering organizational impact (Learn as a team! Don’t create bureaucracy! Move fast! Focus on the customer!) are no matter what kind of organization you run.

A great underwriter possesses many skills: communication skills, analytical skills, administrative skills, sales skills, leadership skills. However, the skill that most differentiates great underwriters from the rest is moral judgment.

Moral codes are our internal rules for how we will conduct ourselves, in good and difficult times. They outlaw certain behaviors and act as a way to credibly signal to others that we can be trusted. Virtue is a value-laden term, it’s an evaluation of one’s moral code against a benchmark of some kind. The virtue that matters for insurance is composed of both the quality of a buyer’s intentions in entering into an insurance contract and also the buyer’s wisdom and experience. It is necessary that the buyer is honest and forthright but it is also necessary that they will not change their character later once they learn some new facts about the world.

The kind of virtue underwriters are evaluating is very specific. There are many forms of virtue and not all relate to the qualities necessary to be a virtuous insurance customer. For example it is virtuous to be a supportive parent, give to charity and be faithful to your spouse. None of these directly matter for insurance. The form of virtue underwriters assess concerns your conduct in dealing with distant financial institutions and whether you will treat them well in the future. This is not a kind of virtue that has existed for all of human history nor one that exists everywhere in the world today. In some ways it’s a very peculiar thing to have a moral code that constrains our actions in dealing with corporations. And we don’t all have it to the same degree.

This is distinct from the work of risk assessment. Risk assessment as insurers undertake it is to assign a risk to its most appropriate segment. Classifying and aggregating risks to determine their costs is an important function of insurance companies but it is not underwriting.

The underwriting of a person or business starts with an assessment of the quality of someone’s intentions, which in a sense is a forecast of that person’s future actions. The most broad and general guide for those actions is morality.

Testing morality works to weed out two different kinds of failures of insureds. First is a group that intends to do something bad1 but is trying to conceal it. As an agent, I once sold a hospital indemnity2 policy to a woman that knew she had cancer and would be going to the hospital in a few days. She somehow got through underwriting (possibly by lying) and filed a claim almost immediately after her policy was issued. I also once saw a trucking customer file a total loss ($1m) at 12:01am on the very day their insurance policy came into force. What did they do wrong? I never found out, but it was very suspicious!

The second is a group that might not intend bad actions now but is especially vulnerable to bad behavior in the future. As a reinsurance broker I had an insurer client that was entering a new line of business. The management team scored high on the integrity scale, they were good people. But when the reinsurance actuaries came into their office for an audit of the pricing model it was clear this group had no idea what they were doing and were systematically mispricing risks in a myriad of ways. They simply were ignorant of how to do their jobs. This is a failure of knowledge and wisdom, not of intentions.

In our daily lives we make judgments of virtue all the time in selecting friends and colleagues and partners of various kinds. In normal life these judgments are heavily influenced by our existing relationships. Moral judgment is a social act. We would have a difficult time accepting or perhaps even understanding the moral evaluations of someone from a very foreign social context or culture. Since our existing relationships share this context they help our evaluation of the virtuous character of another person and offer advice.

Since the evaluation of virtue is so very important, this skill has been the subject of intense competition throughout the history of insurance. And insurers have discovered how to identify and train a talent in certain people so that they don’t need a whole village to pass effective moral judgments: these are the great underwriters.

In normal life moral judgment is a maximizing exercise. Inasmuch as we make explicit decisions about virtue we approve of those who have a lot of it. Over time we probably select lower levels of virtue in our compatriots through implicit processes hidden to our conscious minds, but we are very unlikely to admit that. Moral judgments by great underwriters are all explicit and must contend with the fact that an insurer can make money by selling to people in a whole range of levels of virtue.

Virtue vs Profit

You’ll notice that the slope of the line drops off quickly as virtue declines. The least virtuous are nearly certain to be unprofitable.

But how virtuous do you want your customers to be? Well, to anyone who has taken an economics class, you know where to draw the line.

Easy in theory

But what does this mean operationally? Answering this requires knowledge of both an individual’s virtue and the virtue dynamics of the marketplace. Here’s a question: how virtuous are the customers available to you today through your distribution channels?

Low virtue customers are much easier to acquire than high virtue customers. Partly this is driven by their unprofitability being uncovered by carriers through non-virtuous behavior (and so they get non-renewed from the portfolio). These buyers also work hard at deceiving insurers about their virtue, which doesn’t always work, so they approach many carriers until they slip through.

Flow of customers

The graph above is very surprising. If most available customers are non-virtuous then how is the insurance industry profitable? The confusion comes from mixing up an analysis of flow of customers (above, measured probably in thousands) with the stock of customers (below, measured probably in millions).

Stock of Customers

Most insurance customers do not flow, they are parked inside an insurer’s portfolio, paying their premium every year, filing the odd claim when disaster strikes their lives but mostly making their carrier money. They don’t want to think about insurance and everyone is pretty happy about it. Low churn is a signal (but not a component) of virtuous character. I should be clear, the virtuous can shop too! The non-virtuous are simply overrepresented among shoppers.

Since it is quite hard to get access to a large volume of virtuous customers, underwriters compete on who is better at finding the line and so running a successful business. But as virtue declines deceit increases. There are many insurers that want nothing to do with the minimum virtue zone and focus only on the easiest to underwrite.

Finding the minimum is hard

But only concentrating on the most obviously virtuous people is no free lunch since the competition for these customers is intense. One can underprice the morally straightforward risk as much as the complex and the end of a bout of underpricing is always the same: years-delayed, spectacular financial detonation once the pricing error is inescapably obvious3.

The problem of course comes down to an inability to abstractly measure virtue except after the fact. Carriers that can reliably identify virtuous customers can afford to simultaneously offer better prices, better commission, better service and generate better returns for investors. There are carriers that do just this.

Many innovators seek to eliminate moral judgment with data and clever technology. And there are indeed ways of improving the efficiency of moral judgment. For example, some distribution channels are so incredibly trustworthy4 that underwriting is superfluous and in other instances claims data is so complete and transparent that a person’s behavior can be modeled with incredible accuracy. In these instances underwriting merges with risk assessment and classification. When moral judgment ceases to be an important dimension of competition underwriting ceases to exist.

Villains, however, are always looking to profit from infiltrating unprotected networks and from time to time these lightly underwritten portfolios collapse. When that happens, underwriting by people returns in force to expose the bad hiding among the good. Moral judgment is as complex as humans are clever at deceit.

Having morals as guides for action under uncertainty is a tremendous human achievement and assessing the quality of those morals is an irreducibly human act. For a long time I never really understood what underwriting was. Now I actually think it’s the most deeply human commercial institution we have.

Footnotes

1Doing something bad means finding a way to reliably profit from your insurance policy. Insurance fraud is an example but anything that deceives an insurer into underpricing its policies counts.

3 To pick a price, insurers make an assumption about the claims a portfolio will have. If they get this wrong it usually requires an increase in claims estimates for many years at once, concentrating that cost increase in one financial year. This is the most common way insurers go bust.

4 To pick a price, insurers make an assumption about the claims a portfolio will have. If they get this wrong it usually requires an increase in claims estimates for many years at once, concentrating that cost increase in one financial year. This is the most common way insurers go bust.

This is another installment in my investigation for how to pursue social change. What I notice about insurance is that the institution is so deeply encoded in our society that we don’t even realize how important it is. So deeply encoded that we actually kind of hate it, yet it persists because of how important it is.

What are other ways of pursuing beneficial social change? Persistent beneficial social change? Violent conflict is a pretty big, nasty problem. But what are its roots and what are its causes? What might need to change about our world to reduce it? What is the relationship between peripheral and central societies and how is that related to violence?

All that plus tons on James C Scott and more!

Why did I do this show?

There are a lot of social problems in the world and Chris combines a track record of discovering ways to meaningfully and persistently change very poor societies on some of the most important dimensions. This is very important stuff!

What did I learn?

One of the great things about talking to Chris is a discrete separation of analyzing morality from violence. Sometimes we must sacrifice morals to eliminate violence. Historically, our societies have often had to choose between peace or justice.

What was my favorite part?

In our discussion for how to persistently encode social transformation Chris mentioned the congressional testimony of Fred (Mr.) Rogers. Holy cow.

Clips:

In my conversation with @cblatts we discussed what a world would look like without the tools of war to wage political battles. I kind of wish I could redo this because Chris didn't go as far as I'd have liked. pic.twitter.com/R7kz7Lf9Zq

Paul Ingrey is one of the most successful entrepreneurs in reinsurance history, having started several divisions/reinsurers over his career. He is also an early theorist of the insurance cycle. We need to study more history in insurance!

What was my favorite part?

One of the most amazing things about the very successful people I get to interview on this show is how much they are genuinely good people. This interview captures quite a lot of that quality which was great to experience and re-listen to.

What did I learn?

It’s very, very simple people. The cycle turns only when people are getting fired.

Tyler is an intellectual hero of mine. He’s now a three-time guest! He’s pretty much guaranteed to teach you something every day.

What was my favorite part?

I went 0 for 2 on Straussian readings. Tyler isn’t disagreeing with me, he just thinks I’m being obvious. I shall work harder for the next one!

What did I learn?

The the most important academic result, the one that drives a lot of Tyler’s own work, is that the market test is the most important test of truth. It’s kind of the end of history for academics! At least for those that ignore markets of various kinds.

Howard Kunreuther is the foremost authority on applying behavioral economics to unlikely, high consequence events. I remain astounded that Howard’s teachings are not part of the educational canon for all insurance professionals. This is important stuff! In this episode we discuss:

Cognitive bias and how it impacts society generally and insurance in particular

How we might overcome cognitive bias in our decision making

Prioritization of risk

How politics really is the mediating force for discussing risk

Does voter irrationality give us cause for hope?

Why did I do this show?

Howard is the foremost expert on behavioral economics of insurance. I mean… I still can’t get over how it took me 20 years in this business to learn his work exists. I’m embarrassed this wasn’t my first episode!

What did I learn?

Howard has a lot of ideas for ‘hacking’ our lives to overcome cognitive biases and bring about a better world.

What was my favorite part?

Our discussion of hope. Howard’s bet is that we have genuinely learned things about how humans work that can translate into action and ways to improve the world. Very hard!

Social science is brutally hard to do well. I got one of my guests to admit there has been no progress on it ever and another one to say that moral progress is literally impossible. I think there’s a deeper link to morality and social science than most so this is depressing stuff for me. This episode was part of an effort of mine to get back to first principles. But, uh.. what ARE the first principles of social science? Enter Robin!

What did I learn?

Competition, competition and more competition. That’s the most central concept that Robin uses when reasoning about what might be. Indeed, you may or may not like some cultural feature or another but to predict how successful it will be requires a mechanism for it to be outcompeted in the cultural marketplace. No small feat!

What was my favorite part?

Straightaway we got into a disagreement about generality vs immutability. That was fun. He didn’t convince me I was off base. There was another spot where I disagreed with Robin on speculation about the state of past social science. Again he didn’t convince me! I read somewhere that Robin is ‘not the kind of person you sorta agree with on everything’. It’s such a treat to talk to as creative and deep and original a thinker as Robin.

Why did I do this episode? I first heard about the book from this review by Robin Hanson (podcast guest!) where the authors frame the rise in AI as a drop in the price of prediction. Forecasting is a very important idea to me so I checked it out!

What did I learn? The concept of AI and intelligence generally as a prediction machine is a pretty interesting and useful one.

What was my favorite part? We had a conversation about how useful academic economics and economists are in private companies. A lot of the big tech companies employ economists and one could argue that most cryptocurrency is, in a social sense, an innovation in behavioral economics!