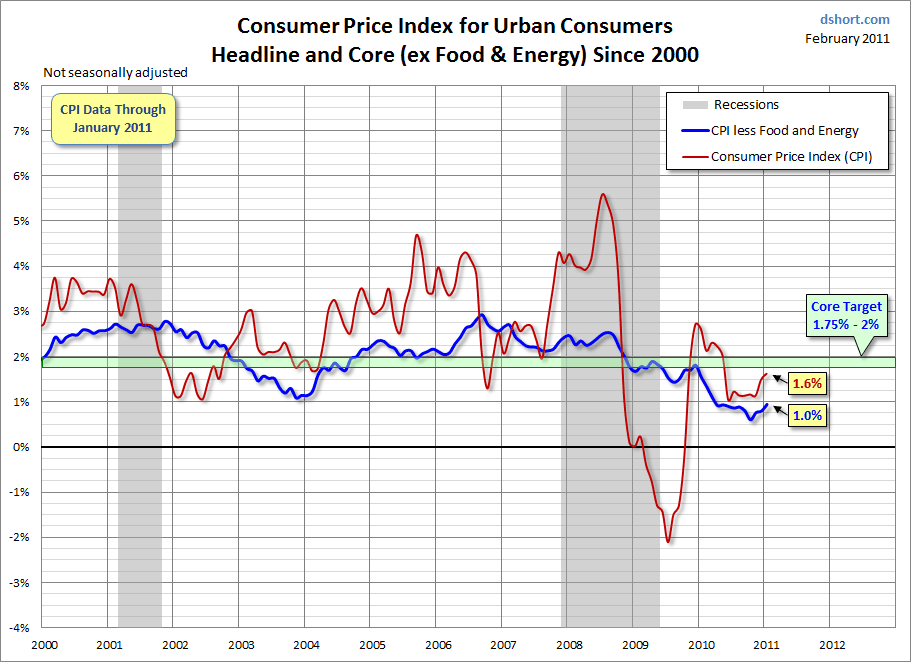

Many people like to look as this graph and freak out:

That monetary base expansion has GOT to mean massive and rampant inflation, right? I mean, Milton friggen Friedman said so!

And for many that means the gold price has to go up (which it has). Yet we have base increase and gold up, but no inflation!

Here is Interfluidity with an answer that, finally, I really really like.

In short, unlike in the 70s, we don’t have inflation because we don’t want it. Surprised? Read on:

The conventional story is that, during a downturn, election-seeking politicians will be recklessly pro-expansion, in conflict with and checked by an independent central bank. But, at least in the United States and Europe, there is surprisingly little appetite among politicians from “mainstream” parties to emphasize either fiscal or monetary expansion. On the contrary, the political conversation revolves around restraining deficits and “being responsible”, which is code for ensuring that the demands of creditors (public and private) are fully satisfied.

This is different from the 1970s, when elected officials did seem to behave as though they were accountable to unemployed people, and put central bankers under intense pressure to be accommodative. Something has changed. In status quo democracies, politicians tend to respond to groups that are numerous, rich, or organized. Since the 1970s, in all the depression democracies, retirees and near-retirees have grown both more numerous (as a fraction of voters) and more rich, while workers have grown less organized. Emerging markets like China have responded to the downturn quite differently. I think this pattern is too systematic to chalk up to idiosyncratic mistakes.

Japan, Germany, and France, more than 50% of the total population is over 40 years old. (56.5%, 57.2%, and 50.2% respectively.) They do have children in these countries, so there are many more retirees and working-age people over 40 than there are younger workers. In the US, “only” 45.5% of the population is over 40, but I think as a polity, the United States behaves as though it is substantially older, because its unusual fecundity (for a developed economy) comes from relatively poor and disenfranchised immigrants. By comparison, China’s over-40 share is 40.3%, Brazil’s is 32.8%, and India’s is 27.1%. In the 1970s, when the US policy was, um, plainly inflationary, the over-40 share of the population was 36.1%.

Using 40-years-old as a cut-off age is arbitrary. “Retirees and near-retirees” is a vague formulation, and 40+ is admittedly a stretch. But people do not turn suddenly into zombie-like asset hoarders. As cohorts of workers age, they accumulate financial assets and become less likely to face unemployment. When they retire, their fear of unemployment disappears entirely, and their dependence upon saved assets increases. There is a continuum between the young and poor, who should prefer the risk of stimulus, and the old and rich who should not. It’d probably be best to modify my story to declare “affluent retirees and older workers” the “median influencer”.