Some Links For Today

In books to watch out for: we have The Benefit and The Burden about taxes. Here is an interesting David Brooks review:

The U.S. does not have a significantly smaller welfare state than the European nations. We’re just better at hiding it. The Europeans provide welfare provisions through direct government payments. We do it through the back door via tax breaks…

David Bradford, a Princeton economist, has the best illustration of how the system works. Suppose the Pentagon wanted to buy a new fighter plane. But instead of writing a $10 billion check to the manufacturer, the government just issued a $10 billion “weapons supply tax credit.” The plane would still get made. The company would get its money through the tax credit. And politicians would get to brag that they had cut taxes and reduced the size of government!

Next we have a follow-up to this (linked to a few days ago) which is Grace Hopper visualizing a nanosecond. Great communicators are awesome. Sends a tingle up your leg, right, Chris?

China’s legislators are shockingly, shockingly rich.

Merkel on Buffett, part 1 and part 2. I haven’t bothered reading the whole letter this year and settled for David’s analysis.

Robin Hanson contemplates turbulence.

The Most Interesting Place On Earth

Might it be Panama?

Geologically the most important landform still around. May have catalyzed human evolution.

Retirement community attracted by the architecture and health care.

Contains the most dangerous place on earth (more here and here).

Oh, and the canal:

Some Links For You

“These are the telephone tapes made by A.J. Weberman of two phone calls (Jan 6th & 9th, 1971) to Bob Dylan regarding an article published by Weberman concerning Bob Dylan. Weberman became infamous for going through Dylan’s trash and selling the garbage he found. I obtained this copy of these recordings from a generation-counting private collector in Ireland 15 years ago and, at the time, I was told they were sourced from a reel to reel copy made from Weberman’s cassettes, rather than from the Folkways LP edition. The material shows amazing insight into Dylan as a human being, a family man and an artist. I decided not to try to clean up the material using DSP since the previous trader left it as he got it.”

Jay Kang of Grantland on Linsanity.

Emphasis for my study tips: work out!

Paul Graham is building a real social network. I envy Y Combinaires (Y Combinatorians? Y Combinatorials? Y Combinastanis?).

Addendum:

Reasons Why Dave Grohl Is Awesome

I am an unabashed fan of Dave Grohl. I don’t have many (any other?) heroes, but this guy effing rocks. Pun intended.

For instance:

I didn’t know the backstory about this song (and it was my immediate fav from that album):

In May 2006, Grohl sent a note of support to the two trapped miners in the Beaconsfield mine collapse in Tasmania, Australia. In the initial days following the collapse, one of the men requested an iPod with Foo Fighters album In Your Honor, to be sent down to them through a small hole. Grohl’s note read, in part, “Though I’m halfway around the world right now, my heart is with you both, and I want you to know that when you come home, there’s two tickets to any Foos show, anywhere, and two cold beers waiting for yous. Deal?”[39] In October 2006, one of the miners took up his offer, joining Grohl for a drink after Foo Fighters acoustic concert at the Sydney Opera House.[40] Grohl wrote an instrumental piece for the meeting, which Grohl pledged he would include on the band’s next album.[41] The song, titled “Ballad of the Beaconsfield Miners,” appears on Foo Fighters’ 2007 release Echoes, Silence, Patience & Grace, and features Kaki King.

There’s this:

And this.

And that’s just stuff I read today.

My first experience watching Dave was at this concert. I can’t tell you the pleasure of owning the dvd of my first time seeing my favorite band. And it was an awesome show. He always puts on an awesome show.

He is too rare a combination of success, work ethic, unaffected empathy, compassion, good humor and unselfconscious charisma.

And I suspect he’d hate to read such sycophantic claptrap about himself.

The good guys can win, too.

Today’s Links

Late night at the office, so while my simulation is spooling up I thought I’d bestow some links upon my readership:

Paging Robin Hanson: Romney watches Intrade:

“If you get on Intrade, Romney has a 73.8% chance of winning the Republican nomination,” Hillsdale College Professor Gary Wolfram said, referring to the popular gambling site which lets users bet on the nomination. “If you really start looking rather than at polls put out by newspapers, if you look at people that are actually looking at this with their own money, he’s in very good shape.”

Interested readers should go here. Obviously this view is fairly self-serving for Romney. Momentum is a well-known self-fulfilling prophecy in politics and any positive spin will be shouted from the rooftops.

That being said, this view confirms my bias, so I’m posting it!

(hat tip to Dane-o)

Tyler Cowen asks Why So Little Money in Politics? Academic literature, not fire-breathing polemics.

Cringely reports Youtube’s big content producers are seeing less hits. Why? A spam-blocking algorithm keeps their stats unpadded. Not surprised. I figure about 85% of the measured visits to this site are complete BS.

Finally, an outstanding metaphor for imagining the speed variation among different computer functions. (these comments have more)

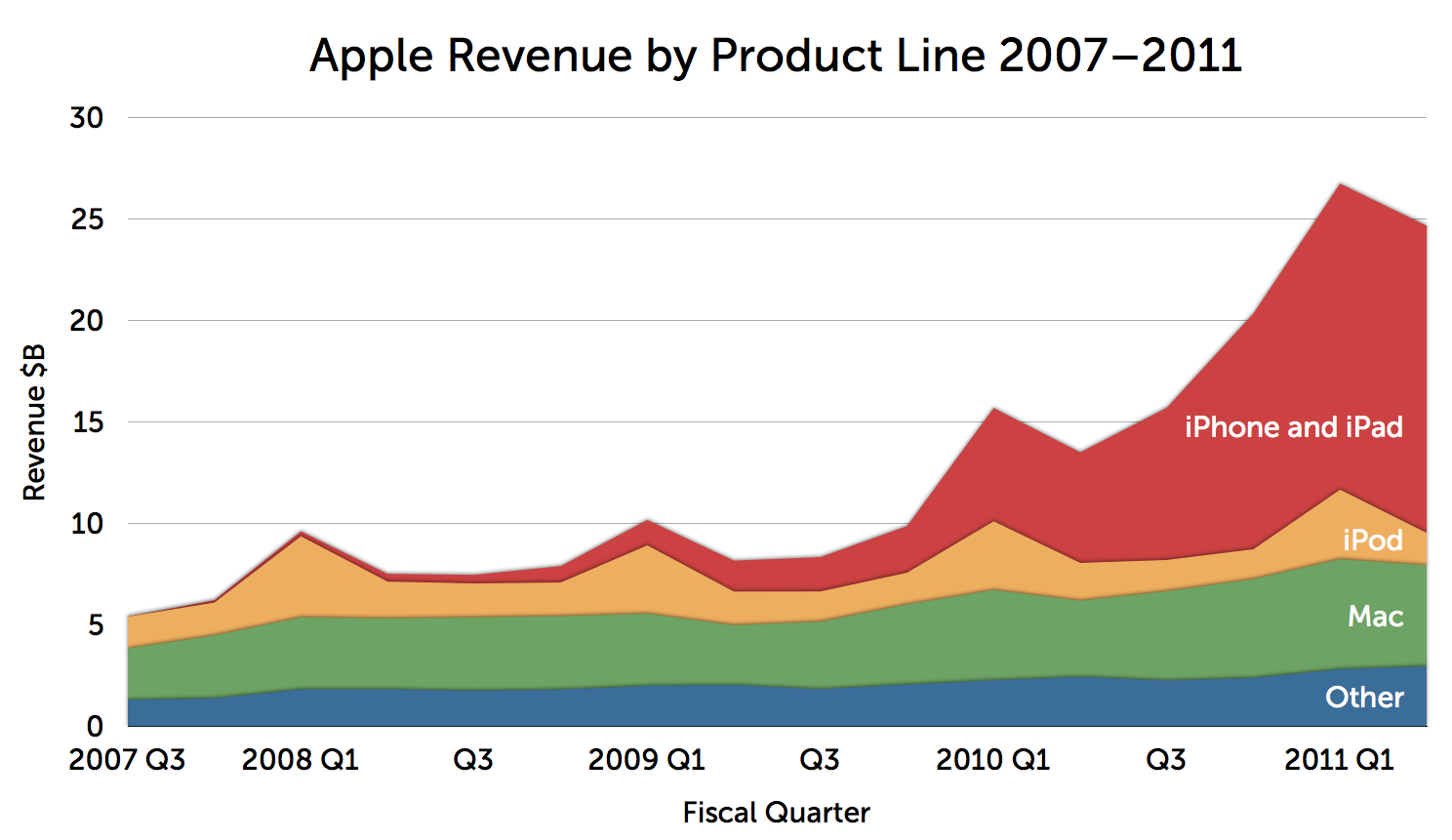

iPhone

I’m slowly figuring out exactly how big of a deal the iPhone has been.

Were Apple’s results stripped out, Barclays Capital estimates earnings growth at S&P 500 companies that have reported fourth-quarter results would be 2.9 per cent rather than 7 per cent.

Wow. Ok, well, Apple’s this awesome company with this gigantic array of awesome products, right?

Apple’s spectacular growth has been down to the iphone (and now, perhaps, the ipad). The rest of the business is about the same as it was. Amazing.

The iPhone is creating a halo for the Macintosh. iPhone has also created a halo for iPad. You can definitely see the synergistic effect of these products, not only in developed markets, but also in emerging markets where Apple wasn’t resonant for most of its life.

Except that growth isn’t about halo effects. Growth is about the next iPhone. This is a product whose success is so incredible I’m not even sure that’s possible!

CAS and CFA Exams – Are They Too Hard?

Jim Lynch reports that the Casualty Actuarial Society (CAS) is undertaking a review of its examination process. The bottom line: some pass rates are too low.

Here is a snip from a letter from the CAS president on the issue, mentioning that this isn’t their first rodeo:

With the agreement of the Vice President – Admissions and the Chair of the Examination Committee, I have directed CAS staff to engage a professional education consulting firm to perform an independent review of our process. A 2001 audit report of the CAS examination process and procedures led to the implementation of the following: (1) development and publication of the learning objectives for each exam syllabus, (2) training of exam item writers, and (3) a content-based pass mark process. The objective of this review will be to evaluate our current processes against best practices for adult professional education.

Jim adds some fascinating detail from the dark ages preceding that 2001 review:

In those days, there was a syllabus and not much else. You memorized its readings – sometimes down to the footnotes – and took the test. There were no rubrics. There was no idea how many points could be derived from any given paper. Without being plugged into the actuarial network – working for a big company, buying an ACTEX manual – you really couldn’t tell what the hell the reading was for, what was important, and how important it was.

Yikes.

Actuarial exams occupy an interesting place in the adult education market. They, along with the CFA exams, are a graduated testing system in which the vast majority of people taking an exam fail. That’s an amazing fact, considering that all of those taking later exams have passed a filter of at least one before. The reason is that later exams are harder.

But I don’t think that these exams are difficult in a Kafkaesque way, with lots of gotcha questions and ‘unfair’ tricks. They’re just trying to shovel a lot of content. The CAS exams, relative to the CFA exams, have a bit of moral high ground here with each level having a defined theme. I found the CFA levels to be a bit more arbitrarily divided.

In both cases, it’s all about the syllabus and its knowledge statements. If you genuinely pay attention to that and follow it, you should be fine. But who’s going to do that?

Much more importantly, these documents allow an industry of outstanding teach-to-the-test organizations (TTTT) to spring up.

The readings supplied with the CAS and CFA exams are abysmal. They’re incredibly difficult to use to actually LEARN stuff on your own. Now, you might say: “why don’t we just tell the CAS to be more like the TTTT companies?” Nope.

These companies are awesome because they need to compete on teaching prowess. In 2008, the CFA Institute forced candidates to buy its crappy books, using its monopoly power to try to force students into an educational stream.

I nearly failed an exam because I felt guilty about buying the Schweser books when I already had the material. I’d argue that the aggregate amount of knowledge gained by candidates went down that year. Is that not the most heinous of outcomes?

So if I had some advice for the CAS and for the CFA Institute (as a member of both), I’d say this: if you’re genuinely concerned about passing rates, the easiest way of getting them up is to double the number of exams and half their content. But that would be administratively painful and I’m not sure you really want to crank up the grades THAT much.

If you’re only concerned about making the exams fair then just work really really hard on the syllabus (with rubrics and knowledge statements and weightings and all the bells and whistles Jim missed out on) and make sure the test is absolutely true to it.

Then back the *#@^ off and let the market teach us.

Will China 2050 be European?

We see massive urbanization driving Chinese development.

Out of the country and into urban service industries. Sounds familiar. So let’s extrapolate.

This paper suggests China’s 2050 population will be roughly the same as it is today.

According to this, overall GDP will increase by between 2 and 2.5x by 2020. By 2050, we’re talking about a 20x increase. China has about 1.4bn people, which will roughly be the same as it was, so the GDP/person will go from something like 1.4b/3t = 4,500 to low teens in 2020 and 90k by 2050?

That means that in 2020 China will be something like Brazil and by 2050 a 1st world country? Sounds like a big jump.

Anyway, I’m thinking more of the rural vs urban divide in China. It’s a densely populated place, even in the rural areas and Ryan Avent taught me that rural and urban differences are deep and deeply political. Urban peoples’ political outlook is hugely shaped by the fact that they live on top of one another and favor more interventionist political systems to deal with all the conflicting interests that result.

The upshot here is that China will have a combination of population density, economic heft and sheer size more similar to today’s Europe than anything else. Will its politics follow suit?

Human Capital Links

Here are some loosely related links:

Ben Horowitz on Andreessen Horowitz’s strategy. The motivating force was his reaction to this:

< That excitement took a sharp downhill turn when one of the top partners said to me, in front of my co-founders, “When are you going to get a real CEO?”

I was completely stunned—the comment knocked the wind out of me. Our largest investor had basically called me a fake CEO in front of my team. I said, “What do you mean?”—hoping he would revise his statement and enable me to save face. Instead he pressed on: “Someone who has designed a large organization, someone who knows great senior executives and brings prebuilt customer relationships, someone who knows what they are doing.”

I could hardly breathe. It was bad enough that he undermined my standing as CEO, but to make matters worse, I knew that at some level he was right. I didn’t have those skills.

But Ben still feels that founding CEOs are still better equipped to run their companies than hired guns. So, as any good founder does, he set out to build a company that squares this circle:

As we set out to design a venture capital firm that would enable founders to run their own companies, we began by asking: In what ways are professional CEOs superior to founder CEOs?

…

Next, we asked: How might a venture capital firm help close those gaps?

Alex Tabarrok gives us this graph, which I’ll let speak for itself for the moment:

Finally, a discussion of consultants. Tyler Cowen gives an interesting take on the ‘why smart kids go into generalist fields’ discussion:

The age structure of achievement is being ratcheted upward, due to specialization and the growth of knowledge. Mathematicians used to prove theorems at age 20, now it happens at age 30, because there is so much to learn along the way. If you are a smart 22-year-old, just out of Harvard, you probably cannot walk into a widget factory and quickly design a better machine. (Note that in “immature” economic sectors, such as social networks circa 2006, young people can and do make immediate significant contributions and indeed they dominated the sector.) Yet you and your parents expect you to earn a high income — now — and to affiliate with other smart, highly educated people, maybe even marry one of them. It won’t work to move to Dayton and spend four years studying widget machines.

You will seek out jobs which reward a high “G factor,” or high general intelligence. That means finance, law, and consulting. You are productive fairly quickly, you make good contacts with other smart people, and you can demonstrate that you are smart, for future employment prospects.

The rest of the world is increasingly specialized, so the returns to your general intelligence, as a complementary factor, are growing too, in spite of your lack of widget knowledge. “Hey you, think about what you are doing! Are you sure? How about this?” often sounds bogus to outsiders but every now and then it pays off and generates a high expected marginal product.

Robin Hanson opens with this:

The puzzle is why firms pay huge sums to big name consulting firms, when their advice comes from kids fresh out of college, who spend only a few months studying an industry they previous knew nothing about. How could such quick-made advice from ignorant recent grads be worth millions? Why don’t firms just ask their own internal recent college grads?

Great questions, and he has some really interesting ideas:

My guess is that most intellectuals underestimate just how dysfunctional most firms are. Firms often have big obvious misallocations of resources, where lots of folks in the firm know about the problems and workable solutions. The main issue is that many highest status folks in the firm resist such changes, as they correctly see that their status will be lowered if they embrace such solutions.

The CEO often understands what needs to be done, but does not have the resources to fight this blocking coalition. But if a prestigious outside consulting firm weighs in, that can turn the status tide. Coalitions can often successfully block a CEO initiative, and yet not resist the further support of a prestigious outside consultant.

To serve this function, management consulting firms need to have the strongest prestige money can buy. They also need to be able to quickly walk around a firm, hear the different arguments, and judge where the weight of reason lies. And they need to be relatively immune to accusations of bias – that their advice follows from interests, affiliations, or commitments.

I like this and it fits with the idea that most consulting isn’t really about giving new or interesting answers to problems. Rather it’s about fleshing out conclusions consistent with the instincts of highly experienced executives. You tend to tell them what they want to hear.

Ok, so here’s why I put all these in one post: I think of the most productive people in society being those with extremely narrow and deep skill sets. That’s where the human capital is. Yet think of many of the highest status folks in our society: the CEOs Ben Horowitz speaks of, the writers, politicians, actors and other professional communicators. They ‘produce’ only relational and cultural consumables and the odd tingly leg.

Nothing earth shattering about all that, I suppose, but many probably scoffed when Tyler Cowen said one solution to The Great Stagnation is to simply raise the status of scientists. Sounds like a good idea to me, if a bit of a long shot.